Expatriation

May 28, 2026

Read more

May 22, 2026

Read more

Apr 12, 2026

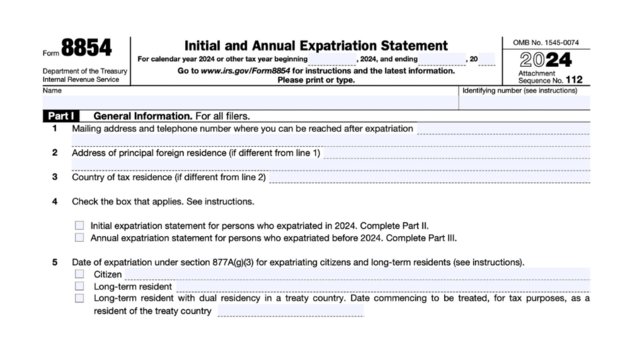

Form 8854 initial and annual expatriation statement instructions: who must file and when

Expatriation

Apr 09, 2026

Read more

Feb 21, 2026

Read more

Aug 10, 2025

Read more