Expatriation

Jul 10, 2026

Read more

Jun 30, 2026

Read more

Jun 12, 2026

Read more

May 28, 2026

Read more

May 22, 2026

Read more

Apr 12, 2026

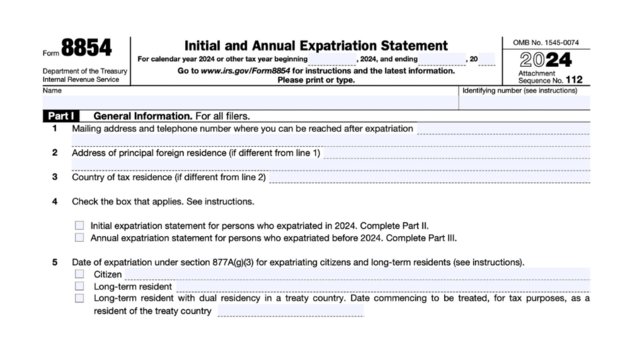

Form 8854 initial and annual expatriation statement instructions: who must file and when

Expatriation

Aug 10, 2025

Read more