The United States has long been the destination of flight students from around the world. Now the U.S. is exporting many of its home-grown pilots as well. The recession and stagnant economy have hit domestic aviation, resulting in many American pilots moving abroad and flying in Asia, Africa and Europe.

We get a lot of questions from pilots who work abroad about their US taxes and decided to put together a brief guide to help you navigate this treacherous field.

If you are a U.S. citizen or a Green Card holder, you are taxed on your worldwide income. This applies whether you live inside or outside of the U.S., or whether you are performing services in domestic or international airspace.

However, U.S. citizens and resident aliens who live and work abroad may be able to exclude all or part of their foreign earned income. In addition, they may also qualify to exclude or deduct certain foreign housing costs.

Meeting the Physical Presence test is a challenge for the pilots. Each day spent on the US ground or over the international waters counts towards the 35 days limit in USA required for the Physical Presence test qualification. Bona Fide test does not have this rigid restrictions and you should use this test as soon as you have spent one full calendar year working abroad.

Provided that you meet the above qualifications, and work on international flights, you may qualify to exclude some or all of your foreign earned income from U.S. income tax, as long as your tax home is in a foreign country throughout your period of bona fide residence or physical presence abroad.

Whether you work as a flight crew member (pilot, engineer, flight attendant) for either a U.S. employer or foreign employer should have no effect on the determination of whether you qualify for the foreign earned income exclusion. The qualifying factor is not the employer type but your Tax Home.

To qualify for the foreign earned income exclusion, your tax home must be in a foreign country. Your tax home is generally located at your regular or principal place of business (unless you have a U.S. abode). If you are a flight crew member, this generally means that your tax home is your base station; the location of the airport from which your flights originate.

However, even if you are based in a foreign country, if you have an abode in the U.S. you will not have a tax home in a foreign country. "Abode" has been variously defined as one's home, habitation, residence, domicile, or place of dwelling. It does not mean your principal place of business and does not mean the same as "tax home”. The location of your abode will often depend on where you maintain your family, economic, and personal ties. Having a U.S. abode will disqualify you from claiming the foreign earned income exclusion.

A U.S. citizen flight crew member based at an airport in Chicago, but residing in Mexico, will be determined to have a tax home in Chicago (regular or principal place of business). Thus, the U.S. citizen flight crew member will not be entitled to claim the foreign earned income exclusion. Alternatively, if the crew member is based at an airport in Mexico, but maintains his abode in the U.S., the individual still cannot claim the foreign earned income exclusion because the individual has an abode in the U.S.

American pilots with a U.S. tax home do not qualify for the foreign earned income exclusion of income earned abroad and do not have foreign credits to offset the U.S. tax. However, there are other means, such as generous per diem deductions and flight crew travel expenses that can be utilized.

If you don’t qualify for the foreign earned income exclusion, you will still be able to take advantage of other deductions. Pilots, flight crew, dispatchers, mechanics, and control tower operators who are under Federal Aviation Administration regulations can deduct a higher percentage of meal expenses while traveling away from your tax home if the meals take place during or incident to any period subject to the Department of Transportation's “hours of service” limits. The percentage is 80%. (vs standard 50% deduction limit). Those deductions can significantly reduce taxable income and lower the final tax bill.

A foreign country is any territory (including its airspace and territorial waters) under the sovereignty of a government other than the United States.

For thе purposes of the foreign earned income exclusion and the foreign housing exclusion/deduction, the terms "foreign," "abroad," and "overseas" refer to areas outside the United States, American Samoa, Guam, the Commonwealth of the Northern Mariana Islands, Puerto Rico, the U.S. Virgin Islands, and the Antarctic region.

The term "foreign country" does not include ships and aircraft traveling in or above international waters.

Earned income is wages, salaries, professional fees, and other amounts received as compensation for personal services. To qualify for the foreign earned income exclusion, the income must be earned in a foreign country. The place where the services are performed determines whether the income is foreign, not the location of the employer or place of payment. For example, if you are a U.S. citizen flight crew member, living and working abroad, receiving wages for services performed in China, those wages qualify as foreign earned income even if you are working for a U.S. airline who deposits your paycheck in a U.S. bank account.

As mentioned above, the term “foreign country” includes its airspace and territorial waters, but does not include airspace over international waters, the United States, U.S. territories, or Antarctica. As a result, income earned for performing services as a flight crew member may need to be apportioned to the actual time spent performing services in a foreign country in order to properly determine the amount of foreign earned income.

Only the portion of income earned for services provided in or over a foreign country is eligible for the foreign earned income exclusion.

A U.S. citizen flight crew member based at an airport in France mostly works roundtrip flights from France to the United States. When working these roundtrip flights, the aircraft flight path generally crosses France, Spain, and Portugal before crossing international waters and entering U.S. airspace. Income earned for providing services in France prior to departure and while flying in French, Spanish and Portuguese airspace is foreign earned income. Income earned for services provided while the aircraft is flying over international waters, in U.S. airspace, and on the ground in the United States is not foreign earned income.

A flight crew member’s earned income is based, in large part, on the services performed from the time the aircraft starts moving away from the gate for departure (“block out” time) until the time the aircraft stops at the gate upon arrival (“block in” time). While the crew member’s earned income is generally computed by the airline based on the actual flight or block time, all of the time spent providing required services (pre-flight, flight, post flight time, training, and other required services) must be taken into account when allocating earned income to the location where they were earned.

We have created this page for tips on tracking flight time and international water boundaries:

https://www.taxesforexpats.com/articles/expat-tax-rules/how-to-track-travel-days-for-us-pilots-flying-international-routes.html

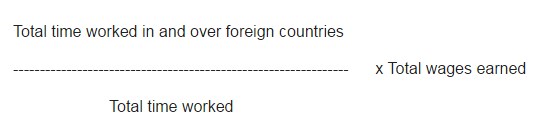

Time basis is used for allocating earned income between “foreign” and “other”. Thus, if you are a flight crew member on international flights, you should be keeping as accurate a record of your hours of service as is possible. In order to compute the amount of your foreign earned income, you will need to compare your time for services performed in and over foreign countries (including their airspace and territorial waters) to your total time spent performing services during the taxable year. This comparison can be expressed by a fraction:

The result is the amount of your foreign earned income (income earned in and over foreign countries, including their airspace and territorial waters).

Vacation pay and sick pay are included as total wages earned. Thus, vacation pay and sick pay are allocated between “foreign” and “other” based upon the actual time spent performing services in foreign countries and in other places. However, used vacation time and sick time do not go into the numerator or denominator of the fraction outlined above.

The IRS regulations have obscure spots. Lack of clarity leads some accountants to conclude that international waters begin three miles off the coast, while others say the boundary starts 200 miles offshore.

Because flight time between two cities may vary based on the actual flight route, location of the jet stream, weather, and other factors, the most accurate way to determine the time spent in and over foreign countries is by using detailed records (flight plans) for each flight reflecting the flight’s planned route and the planned flight time. The flight plan includes a lot of information about the flight, including the route designated by its latitude and longitude readings as well as the estimated flight time between those points. The flight plan will also show the total estimated flight time from the flight’s block out to its block in. As a result, it is possible to plot the geographical points and determine the actual planned time spent flying over foreign countries.

There may often be difficulty securing and reading actual flight plans. This process is burdensome for crew members who fly a large number of international flights during the taxable year.

Don’t overlook a valuable time saving tool: many airlines are providing crew members a breakdown reflecting the “average” flight time components of flight segments in and over foreign countries (sometimes called “Duty Time Apportionment” or “Flight Time Apportionment”). These apportionments, if reasonable, are acceptable as a means to determine the amount of foreign earned income.

We hope this guide was useful in clearing up some complex tax issues that American pilots working overseas encounter.

We’d be happy to assist with your tax preparation or questions - stop by our website: www.taxesforexpats.com or send us an email to success@tfx.tax.