Expat tax services from trusted tax experts

Over 4,000+ reviews

Mentioned in

We make it easy for you

-

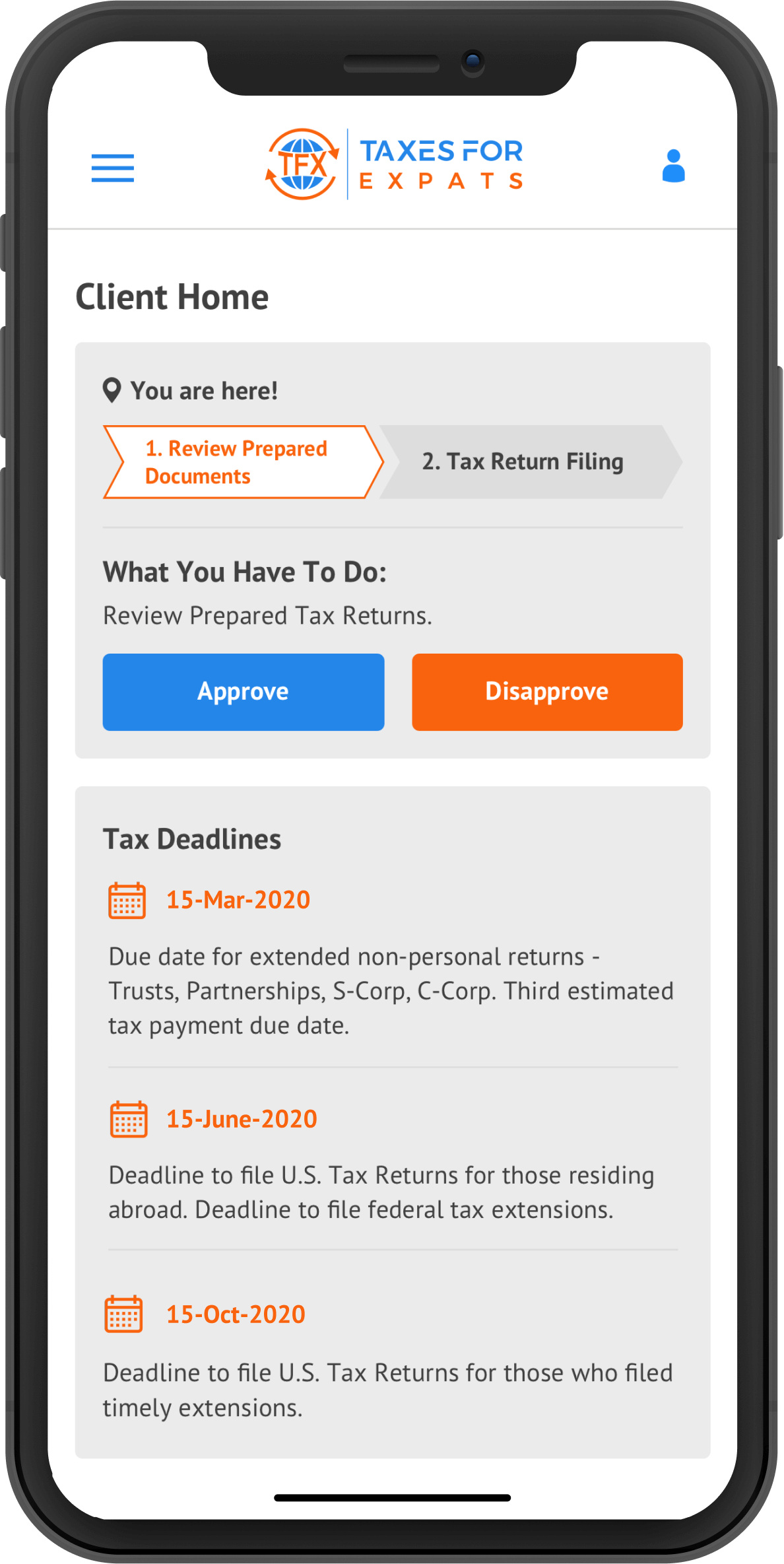

Create

an account -

Complete

Tax questionnaire -

Sign

Engagement letter -

Sit back

while we work -

Pay

and review

Expert, human accountant working on your case

Professionals who care & stand ready to answer your questions. Experienced humans who understand expat taxation in and out.

80+ accredited CPAs, EAs, JDs.

Real people, just like you.

50,000+ clients, 193+ countries, 4,000+ reviews

Articles & tax guides

View all →What is Form 14653? Form 14653 is the IRS certification form u...

The Internal Revenue Service introduced the ...

Viele Amerikaner, die in Deutschland leben, stellen Jahre später fest, dass von ihnen immer noch erwartet wird, US-Steuererklärungen abzugeben, ausländische Bankkonten zu melden und die internationalen Meld...

“I am completely at ease now – TFX made it ver...

Your 401(k) usually stays open when you move abroad, and a US citizen does not become a foreign payee just because of a foreign address. The real changes are practical and tax-related: employer-plan access, future contrib...

US citizens and resident aliens abroad must report foreign self-employment income on a US tax return when they meet the filing rules for the 2025 tax year. The key issue is that self-employment tax on foreign earned income is separate from income tax, even when the Foreign Earned Income Exclusion (FEIE) reduces taxable income on Form 1040. ...

Data secured by

two-factor authentication

Access to your information anytime, anywhere