FREE TAX EXTENSION

Extend your tax deadline to October 15 in minutes – avoid late filing penalties.

At TFX we've been doing taxes for U.S. expats for over 25 years

Expat taxes are complicated. Seriously.

Every precaution recommended by the IRS. And then some

Clear, transparent process. Thorough & well-thought-out

IRS Restructuring & reform act of 1998 protects taxpayers

Trusted by tens of thousands of clients worldwide

Which should you hire and why?

Join a leading expat tax firm trusted by clients around the world

Join a leading expat tax firm trusted by clients around the world

Many imitators, only one TFX. Ask the tough questions

Specific use cases & scenario analysis

Top notch customer service is core to TFX

We are the best at what we do and we're here to help you

Start your tax prep in minutes – simple and hassle-free

IRS amnesty program for expats with overdue returns

For non-US citizens or Green Card holders with US income

Selling stocks? Changing jobs? Plan your taxes early

Get 6 extra months to file – quick, easy, and penalty-free

20 min call to assess your needs and next steps

IRS amnesty for US-based taxpayers behind on filings

Fix past returns and refile with accurate corrections

We’ll decode and respond to IRS letters for you

Expat? Extend your tax deadline until December 15

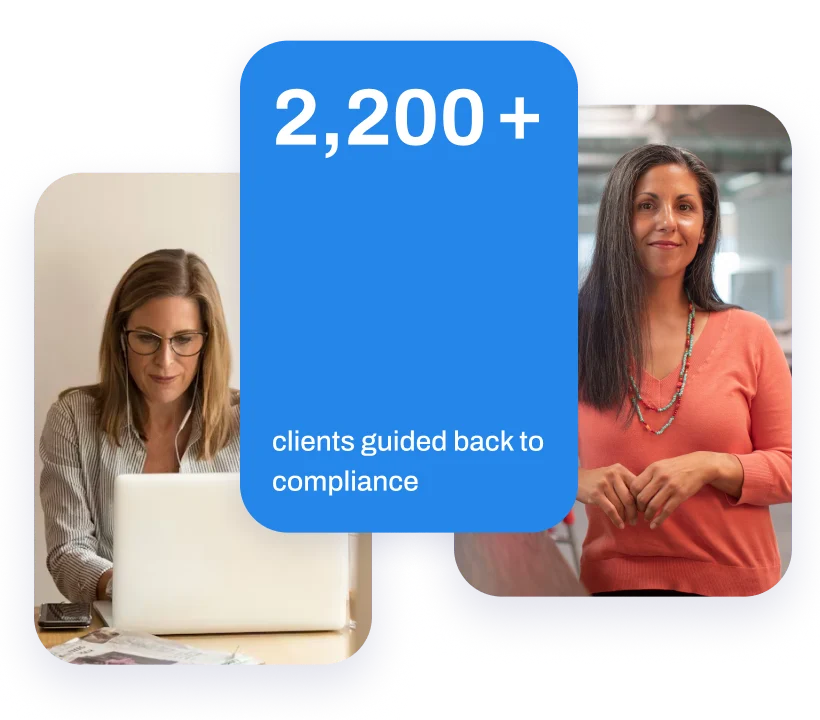

2,200+ streamlined submissions

Proven experience resolving multi-year non-compliance cases.

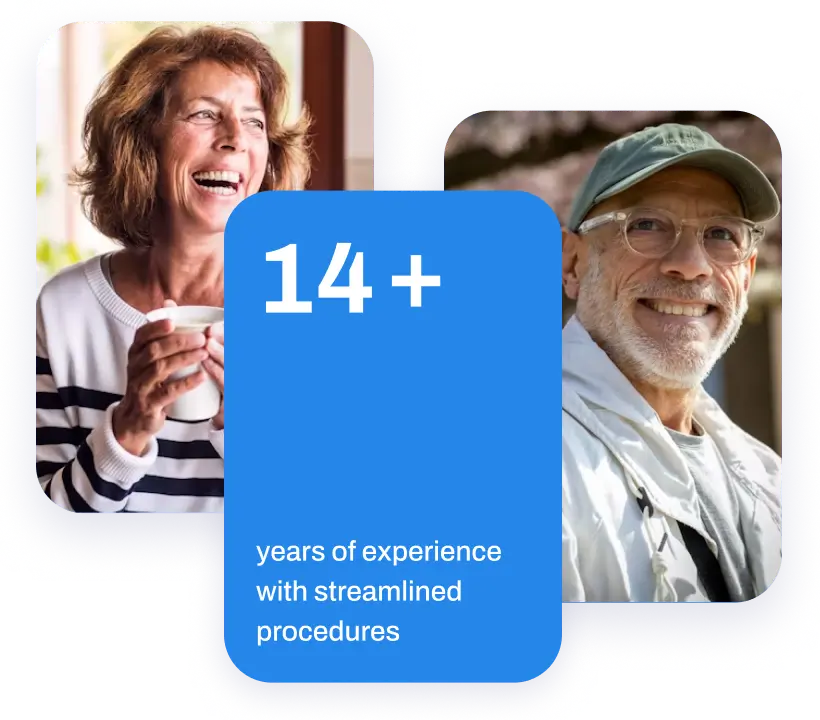

Streamlined specialists since 2012

Deep expertise in expat and cross-border filings.

Structured accuracy system

Preparation → second-level CPA review → final compliance check.

3 federal tax returns + 6 years of FBARs – handled end-to-end for penalty-free compliance.

Your case is handled by expat CPAs specializing in non-compliance and cross-border tax filings.

We prepare 3 years of delinquent or amended US returns as one coordinated, streamlined submission.

We prepare and file 6 years of FBARs for qualifying foreign accounts.

We draft your non-willful certification (add-on) based on your facts, aligned with IRS expectations.

Upload documents and communicate securely with your assigned CPA through our system.

You've been overseas for years and only recently realized the US requires annual tax returns and foreign account reporting.

You discovered you have US tax obligations – even though you've lived most (or all) of your life outside the US and were unaware of the filing requirements.

You filed taxes where you live and assumed that was sufficient – not realizing that US citizenship carries separate annual tax return and foreign account reporting obligations.

You hold a green card or meet US residency rules, and didn't realize that status comes with annual filing and foreign reporting requirements.

Streamlined Procedures are available to taxpayers who come forward voluntarily and meet eligibility requirements. Addressing non-compliance before the IRS initiates contact helps preserve eligibility for Streamlined Procedures.

Start with a consultation to review your situation and understand the next steps toward resolving non-compliance.

Our tax specialists assess your situation to determine the correct streamlined filing path before preparation begins.

Upload your records through our secure client portal. We guide you through what’s required, so you know exactly which documents to provide and don’t feel overwhelmed by the process.

Your CPA, specialized in Streamlined Procedure, prepares your required tax returns, FBARs, and non-willful certification (if added) as one coordinated submission.

Our CPA streamlined filing process follows a structured preparation and review system to ensure accuracy and full alignment before submission.

After your approval, your streamlined package is submitted and we remain available for any necessary follow-up and streamlined filing assistance.

If your income exceeds $100,000, the package cost is adjusted to $1,650.

| Service | Price |

|---|---|

| Preparation of non-willful certification for expats | $300 |

| US paid preparer certification for bank compliance | $150 |

A proven system that has brought thousands of Americans back into compliance.

14 years of hands-on experience structuring accurate, multi-year submissions.

Preparation by a CPA specialized in Streamlined Procedures → second-level CPA review → final compliance check before submission.

Establish a clean baseline so future filings become simpler and more predictable.

Our streamlined filing assistance is a flat fee of $1,450 ($1,650 if your income exceeds $100,000), with no hidden fees.

Optional services include:

We prepare and file 3 years of federal tax returns and 6 years of FBAR reporting. Your package also includes an eligibility review and CPA help. We handle all required reporting as part of our IRS streamlined foreign reporting services for qualifying taxpayers.

Yes. We review your situation upfront to confirm eligibility for the Streamlined Procedure and determine the correct filing path beforehand.

Your case is handled by CPAs experienced in non-compliance and cross-border filings, following a structured preparation → second-level CPA review → final compliance check process.

Timelines depend on how quickly documents are provided. Our workflow is designed to move you from non-compliance to confident compliance efficiently and accurately.

Yes. We determine the correct approach based on your residency and filing history before submission.

You'll need income records and foreign account details for FBAR reporting. We guide you through document submission so your filing is complete and consistent.

Start with a consultation. We'll review your situation and outline the next steps to resolve your non-compliance.